As with the close of every financial year, the ATO has announced changes to the way superannuation contributions are managed and governed. Most of these changes are effective from 1 July 2020 so it’s important to get across them and understand how they affect your individual financial situation.

This article will take you through the main superannuation contributions rules and changes including:

- Concessional and Non Concessional Contributions caps

- Work test rules

- Excess contributions

- Carry-forward unused concessional cap

- Downsizing after age 65

- Capital gains tax small business concession contributions

- Government co-contribution

- Low-income super tax offset

- Claiming tax deductions for personal super contributions

- Contributions tax for higher income earners

- Superannuation Guarantee (SG)

- Spouse contribution splitting

What are the Superannuation Contributions Caps?

Contributions caps apply to the superannuation contributions you can make to your super fund each financial year. While you can contribute more than the cap, you’ll likely be required to pay additional tax. The amount of tax you pay depends on the type of contribution.

Concessional contributions

Concessional contributions are made into your super before tax and are generally; compulsory employer contributions, salary sacrifice or personal contributions for which you have claimed an income tax deduction.

From 1 July 2020, the concessional contributions cap is $25,000 for the year, regardless of your age. If eligible, you may wish to consider the 5-year rolling catch-up contributions if you have less than $500,000 in super at the start of the financial year.

Non-concessional contributions

Non-concessional contributions are made into your super fund from your savings or from income that you’ve already paid tax on, which means they’re not taxed when received by your super fund.

From 1 July 2020, the non-concessional contributions cap is $100,000 for the year. Note that you can’t make non-concessional contributions if you have a total super balance over $1.6 million at the start of the financial year. If certain criteria are met, you may wish to utilise the 3-year bring-forward rule.

What are the Superannuation Work Test Rules?

The superannuation work test was put in place to allow people over the age of 67 to continue contributing to their superannuation fund if they satisfied the requirements.

From 1 July 2020, the age for the work test was increased to 67. The work test requires that you have been gainfully employed for at least 40 hours in no more than 30 consecutive days in the financial year.

You must satisfy the work test prior to the contribution being made, although this does not apply to downsizer contributions. If you are aged 67 to 74, a work test exemption applies for 12 months from the end of the financial year in which you last met the work test, provided your Total Superannuation Balance is less than $300,000 at the prior 30 June and you have not previously used this exemption (it can only be used once).

How are Excess Contributions Treated?

Excess contributions are the payments you make into your super fund above the contributions caps. When this occurs, you’re charged extra tax, which can be quite high in some cases! The way excess contributions are treated depends on:

- Your age

- Whether the contributions are concessional or non-concessional

- Which financial year the contributions relate to

Excess concessional contributions

The excess is counted as personal assessable income and taxed at your marginal rate plus some additional charges, received as a tax offset to reflect the 15% tax paid on these contributions by the super fund. You can elect to withdraw the excess from your fund but, if you elect not to, it will also count towards your non-concessional contribution cap.

Note that these rules have changed several times in recent years so this treatment will not necessarily be applicable for concessional contributions you have made in the past.

Excess non-concessional contributions

The excess is taxed at 45% plus 2% for Medicare; however, before levying this tax, the ATO will give you the option of having the excess contributions plus a notional amount (calculated

by the ATO) to reflect investment earnings refunded to you.

Instead of being taxed the whole amount of the excess at the very high rates mentioned above, you may elect to refund and pay tax on the notional earnings. These will be taxed just like normal personal income, less a 15% tax offset.

What happens if I make an excess contribution?

If you contribute superannuation above the contributions cap, you’ll receive a letter from the ATO identifying the excess contributions. At this stage you can either:

- Elect to pay additional taxes personally

- Elect to have the money released from super by completing the appropriate form and returning it to the ATO (This is available through MyGov or your accountant). It is important that no money is released from the superannuation fund at this step.

The ATO will process the form and send a release authority to the superannuation fund. The superannuation fund must then release the money to the ATO within 21 days alongside a form documenting the release.

The ATO will process the release, deduct any additional taxes (above the 15% already paid by the super fund) and release any residual amounts back to you as though it were a personal tax refund from the ATO.

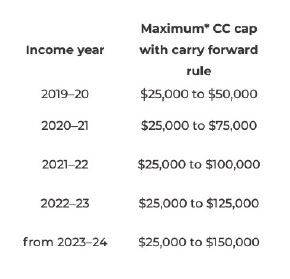

What are the New Carry-Forward Unused Concessional Caps?

From 1 July 2018, individuals are able to carry forward their unused concessional cap for up to 5 years for use in a future financial year.

In this case, an individual’s concessional cap can be increased if:

- The actual concessional contributions are greater than the standard cap

- The total superannuation balance is less than $500,000 at 30 June of prior financial year

- The individual has an unused concessional contribution cap available from any or all of prior 5 financial years (occurring from 2018/2019 FY onwards)

Making Downsizer Contributions Over the Age of 65

If you’re over 65 years of age and have owned your house for at least 10 years, either you or your spouse can claim a full or part main residence exemption when you sell your house. In these circumstances, both individuals can contribute up to $300,000 each to super as a non-concessional contribution, which doesn’t count towards the non-concessional contribution cap. Note that the contribution can’t be greater than the sale value of the home.

When you sell your home to make a downsizing contribution, there is no requirement to purchase another home and you can still make the downsizer contribution if you have a Total Super Balance over $1.6M. To apply this strategy, you must complete the Downsizer Contribution into Super Form (NAT 75073), which can be downloaded from the ATO website: https://www.ato.gov.au/Forms/D... is the downsizer contribution eligibility criteria?

- You’re 65 years or older at the time you make the contributions (no maximum age limit).

- The home was owned by you or your spouse for 10 years or more prior to sale (the ownership period is generally calculated from settlement of purchase to the date of settlement of sale).

- The home is in Australia and is not a caravan, boat, or mobile home.

- The home was either exempt or partially exempt from CGT under the main residence exemption.

- You provide the downsizer contribution form to your super fund (before or at the time contributions are made).

- You make the contribution within 90 days of the date of settlement.

- You haven’t previously used the downsizer contribution cap.

Updates to the Small Business Capital Gains Tax Concessions

If you run a small business, you might be eligible for capital gains tax concessions on the sale of assets you use to run your business. Generally, there are two provisions under the small business capital gains tax concessions that allow for sale proceeds to be paid into super, so long as special conditions are satisfied.

- 15-year exemption:

- If you’re aged 55 or older and are retiring or are permanently incapacitated, and you have owned an active business asset for at least 15 years, you won’t pay capital gains tax when you dispose of the asset

- Amounts from this exemption may be contributed to your super fund without affecting your non-concessional contributions limits.

- The 15-year exemption contributions now count towards the $1,565,000 lifetime limit.

- Retirement exemption:

- There is a capital gains tax exemption on the sale of an active business asset, which is now capped up to a lifetime limit of $500,000. If you’re under 55, money from the disposal of the asset must be paid into a complying superannuation fund or a retirement savings account.

- Amounts from this exemption may be contributed to your super fund without affecting your non-concessional contributions limits.

- When using this exemption, the contribution still counts towards the $1,565,000 lifetime cap.

It’s important to note that this approach is confirmed using the ATO form no later than the time when the contribution is made. Contributions are treated as non concessional contributions in the super fund and different timing rules apply for each one. Additional conditions do apply so financial advice is highly recommended when considering these types of contributions.

Accessing the Government Co-Contributions Scheme

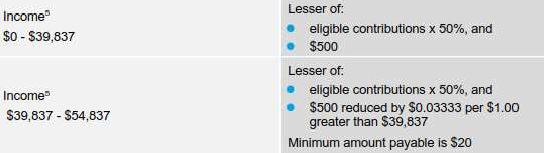

As you know, if you’re a low to middle-income earner, you can boost your retirement savings by making personal (after-tax) contributions to your superannuation fund. When this occurs, the government may also make a contribution to your fund to support your savings up to $500. The amount the government contributes depends on your income and your contribution.

Are you eligible for government co-contributions?

Personal non-concessional contributions can be made to a complying fund where individuals have not exceeded their non-concessional contributions cap. Individuals must pass the Minimum Earning Test, whereby 10% or more of your income comes from business or employment.

This is calculated as:

You must also meet the following criteria:

- Your tax return for financial year must be lodged

- You must be less than age 71 on the last day of the financial year

- You mustn’t hold a temporary visa at any time during the financial year (unless you’re a New Zealand citizen or it was a prescribed visa)

- You can’t have more than $1.6 million as at 30 June of the prior financial year

- Your income* must be less than $54,837 (*Assessable income plus RESC and reportable fringe benefits total less business related deductions)

The amount payable calculated as:

Rules of the Low Income Super Tax Offset

The Low Income Super Tax Offset (LISTO) is a government superannuation payment of up to $500 to help low-income earners save for retirement. If you earn $37,000 or less per year, you may be eligible to receive a LISTO payment, which is paid directly into your super fund.

The payment is 15% of the concessional (before-tax) super contributions you or your employer pays into your super fund. The maximum payment you can receive for a financial year is $500, and the minimum is $10. You don’t need to do anything to receive the payment.

You’re eligible for the LISTO payment if:

- You have made concessional contributions into a complying fund

- Your adjusted taxable income is less than $37,000

- You have fulfilled the Minimum Earning Test, whereby 10% or more of your income comes from business or employment (see section above for more)

- You have lodged your tax return for the financial year

- You don’t hold a temporary visa at any time during the financial year (unless you are a New Zealand citizen)

Claiming Tax Deductions for Personal Super Contributions

From 1 July 2017, the “10% Test” was removed, meaning that more individuals may now be able to claim a personal tax deduction for making personal concessional contributions to their super fund. Note that a deduction for a personal contribution cannot result in or add to a tax loss.

You’re eligible to claim a tax deduction if you made a personal concessional contribution to your super fund and meet the following criteria:

- You were at least 18 years of age or more when the contribution was made (unless you’re deriving income from carrying on a business or engaging in employment-related activities)

- You made the contribution within 28 days of turning 75

A valid notice of intention to claim a tax deduction, in an ATO-approved form, must also be given to the fund trustee within a certain timeframe. A notice can’t be revoked or withdrawn but it can be varied to reduce the amount claimed. Your notice must be lodged with your super fund before the earlier of:

- Lodgement of your tax return for the year contributions were made

- The end-of-financial year after the financial year during which the contributions were made.

To maintain eligibility, the trustee of the fund must acknowledge the notice.

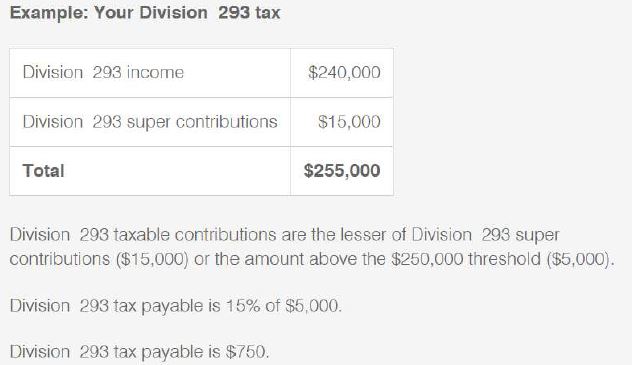

Superannuation Contributions Tax for Higher Income Earners

Division 293 tax is an additional tax on super contributions, which reduces the tax concession for individuals whose combined income and contributions are greater than the threshold. The way it works is that an additional 15% tax is charged on an individual’s taxable contributions when their income for 2020/21 FY is $250,000 or above.

Your income is assessed as Division 293 income based on the sum of your:

- Taxable income (assessable income minus allowable deductions)

- Total reportable fringe benefit amounts

- Net amount on which family trust distribution tax has been paid

- Net investment loss

- Net rental property loss

If your income exceeds $250,000, an additional 15% tax applies to the lessor of your:

- Income above $250,000

- Low-tax contributions (eg. Excess concessional contributions)

Not sure how you will know if you have to pay Division 293 tax? The ATO will send you a notice of assessment once they have received both your income and contribution information for the year.

Here's an example:

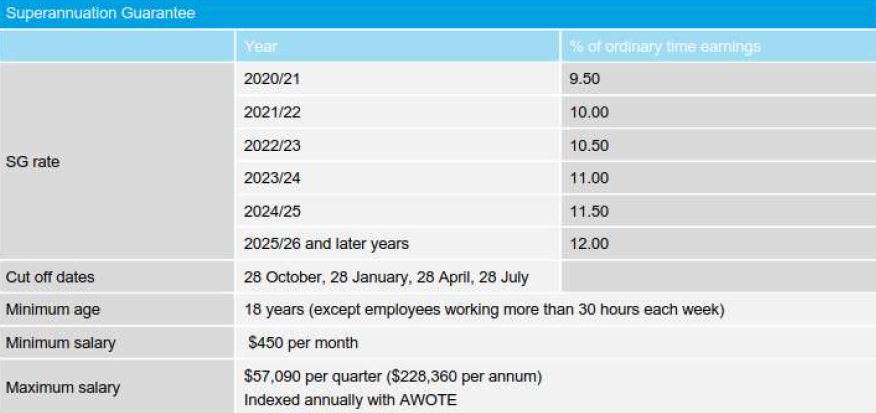

Superannuation Guarantee (SG)

Spouse Contribution Splitting

Contribution splitting allows you to split your concessional (before-tax) contributions from your accumulation super account with your spouse. Some advisors use this to level out member balances between husband and wife.

The application must be lodged with the super fund within the financial year after the financial year in which the contributions were made, or in the financial year of the contributions made, if your entire benefit is being rolled over or withdrawn.

The maximum splittable amount is the lessor of:

- 85% of your concessional contributions

- Your concessional contributions cap for the year

- The taxable component of your interest.

In the case of spouse contribution splitting, the contribution is treated as a rollover into your spouse’s account and doesn’t count towards either the concessional contribution cap or the non-concessional contribution cap of the receiving spouse. It is classified as a 100% taxable component into the receiving member’s account. Only one contribution split can be made per financial year.

The receiving spouse must not be:

- aged 65 years or more

- aged between the preservation age and 65 and ‘retired’.

We hope you found this information on superannuation contributions useful and interesting. If you would like advice on your superannuation contributions strategy or have specific questions for an expert, feel free to get in touch with our superannuation specialist, George Karavias at george.karavias@thebluerock.com.au or Contact Us .

Disclaimer

The information contained in this article is factual in nature and should not be taken as advice. The information is taken to be correct at the time of writing; however, may change over time and should not be relied upon. You should always check for any changes to the law. We also, highly

recommend you seek professional advice from a certified financial advisor prior to making any contributions to your superannuation fund.